An insurance cover is often not as simple as it sounds. With the growth of the internet, there is a variety of insurance coverage available to compare in the market. They offer different types of offers and discounts. And because of these lucrative offers sometimes we miss out some of the important aspects of what we are buying. The Insurance Regulatory and Development Authority ( IRDA) has also laid down some attributes of a smart policyholder.

At the time of buying the policy:

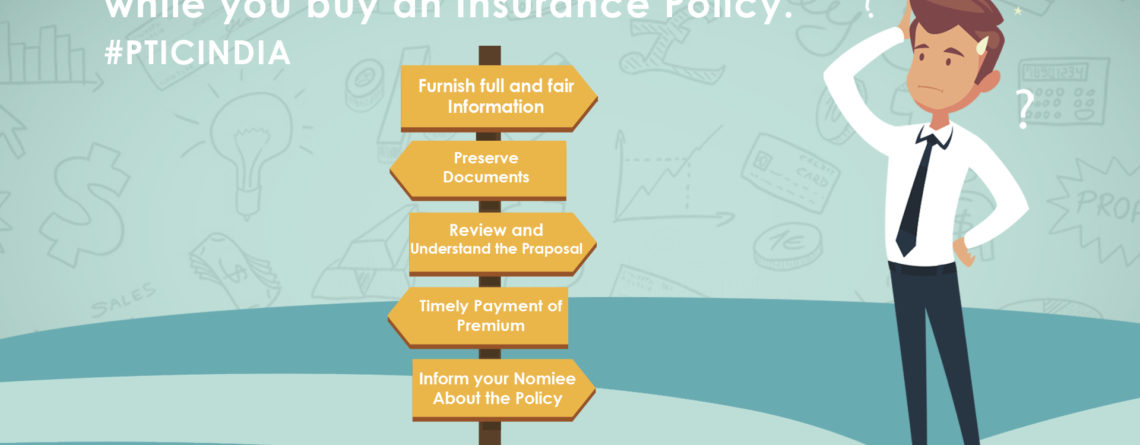

- Fill in the proposal form with good faith in the insurance company. It means to give your inputs correctly and truthfully; it is the basis of the insurance contract. One should not leave any column blank or empty or never sign a blank proposal form. You are going to be responsible for any information in this document as it bears your signature.

- Disclose all material information about the risk you wish to cover.

- Select the term of the policy as per your needs, select the mode of the premium payment- single or regular payment- and the premium amount you can afford to pay.

- Register nomination under your policy and fill the nominee’s name correctly.

Before buying any policy, in case of a general insurance plan, compare the Insured Declared value you are getting. The claim settlement ratio and the process being followed by your insurer also need to be compared.

A health insurance policy safeguards you and your entire family in times of medical emergency. Before buying a health insurance plan, assess the kind of policy and specific requirement etc number of people to be covered, sum insured depending on the medical history and age of the insured members. Another important aspects to mull over are hospital network and accessibility, pre and post hospitalization expense allowances, inclusions, and exclusions.

After you buy the policy:

- Once the proposal submit, you should hear from the insurance company in 15 days. If you don’t, take up the matter in writing. And if any additional documents are asked for, then comply immediately.

- Once the proposal accepted by the insurance company, the policy should reach you within the reasonable time. If not, contact the insurer.

- When the policy bond is received, check it and be sure that the policy is the one you wanted.

- After receiving a policy, make sure to make a note of the policy issuance date. If at all you have to return the policy to the insurance company, recording this date will help you keep a track of the free-look period which is usually 15 days.

- Read the policy documents and ensure that you were made aware of all that is explained by the agent or other intermediary or insurer directly at the time of sale. If doubts crop up, then contact the insurer or agent immediately for clarification.

- Keep a copy of the policy with you and inform your family members about the policy details.

Maintaining the policy:

- Pay your premium regularly on the due dates or within the grace period

- Don’t wait for a premium notice for making payments. Pay it on time to avoid policy lapse or other penalties.

- In case of change of addresses, change of the usage of the assets etc intimate the insurance company at the earliest.

- You can change your nominee after the policy issued to you. By filing a notice of change of nomination and sending the same to the insurer.

- Renew your policy before it expires. If there is a gap in insurance beyond 90 days then you can end up losing your No claim bonus.

- Make sure you complete your KYC details before in hand

- Don’t lose a copy of the insurance policy document. Without a proof, it can be difficult for your beneficiaries to collect any benefits.

At the time of a claim:

The first step to avail an insurance claim is to email a completely-filled claims settlement form. Different claims need different sets of documents. Make sure that all the necessary documents are in place while submitting the claim settlement. Whenever required, you should help the insurer in the prosecution or for recovery of the claims which the insurer has against the third party. For smaller claims, ask the insurance company if it would be better if you retain you NCB or make a claim. Customers should be aware of the claim process in order to enjoy the complete benefits of the policy so thoughtfully purchased. This includes knowledge of the network hospitals, cashless claim process, possession of the customer ID and other details for seamless admission, among other things.